PRODUCTIVITY

CALCULATOR

WHAT IS PRODUCTIVITY?

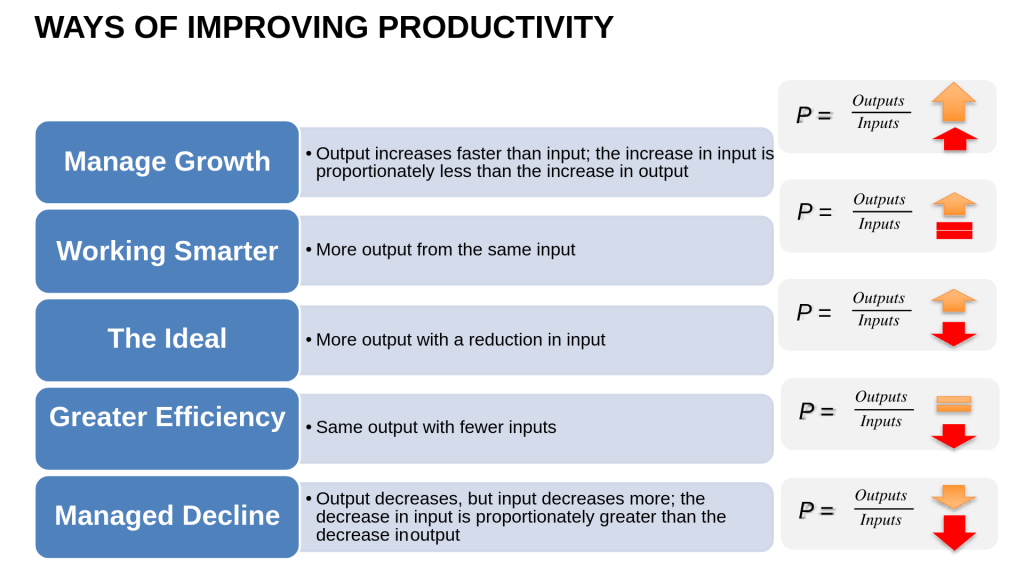

Productivity measures the efficiency of input in producing the output. It is simply calculated by dividing the output/input.

Output refers to end-product of the process which can either be the finished goods or the services rendered.

Input refers to the amount of resources that are utilized in producing the goods or in providing the services.

| Output | Input |

|---|---|

| Gross Domestic Product (GDP) | Employees |

| Total Output | Total man-hours worked |

| Value Added | Labour Cost |

| Monetary Value of Production | Capital/Fixed assets |

| Quantity of physical unit produced | Energy |

| Net Sales | Material |

| Services |

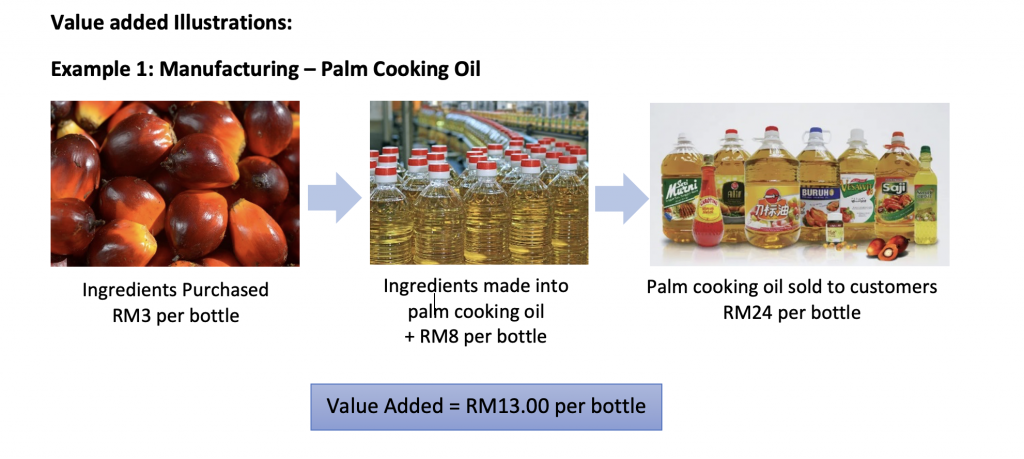

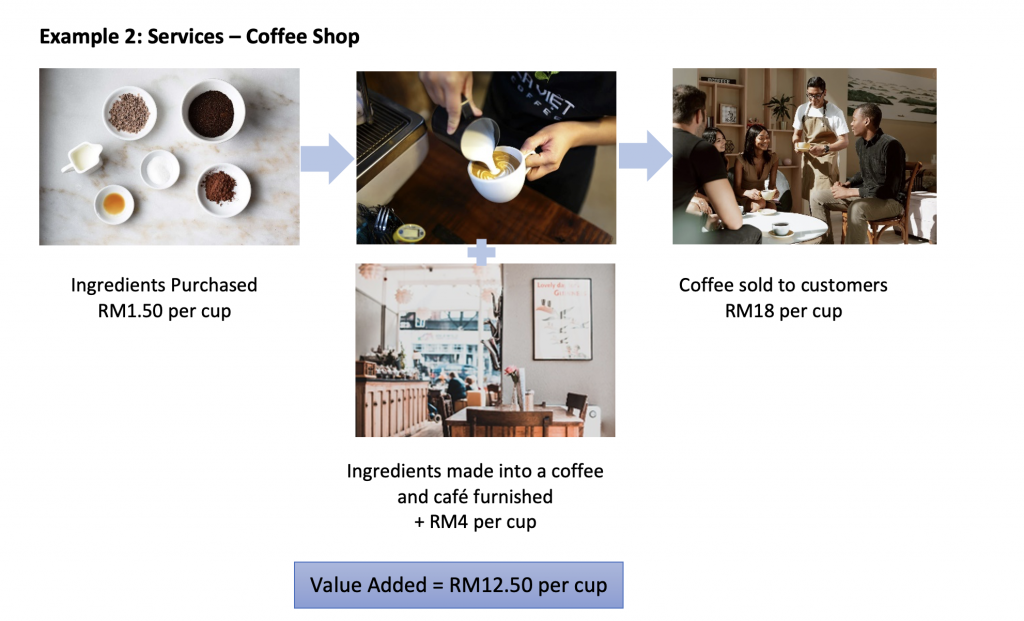

Value added is the additional features or economic value that a company adds to its products and services before offering them to customers. Adding value to a product or service helps companies attract more customers, which can boost revenue and profits.

Sources of value added – Branding, Quality, Convenience, Speed, Design, Unique Selling Point

Using value added in measuring productivity reflects the amount of wealth created by the industry, relative to the number of input it has such as employees or fixed asset.

Labour Productivity can be calculated by measuring the number of units produced relative to employee or by measuring a company’s value added relative to employee.

Capital Productivity measures number of units produced or value added, relatively to capital or fixed asset.

Please contact MPC for further clarification

- Delivery Management Office dmo@mpc.gov.my

- Dr Mazlina Shafi’i eyna@mpc.gov.my

- Asmawadi Mohamed asmawadi@mpc.gov.my